Micah Jonah

March 16, 2026

Rapid expansion of fintech in Nigeria is driving authorities to tighten anti-money laundering (AML) measures, with the Central Bank of Nigeria (CBN) mandating automated AML systems across banks, mobile money operators, and other financial institutions.

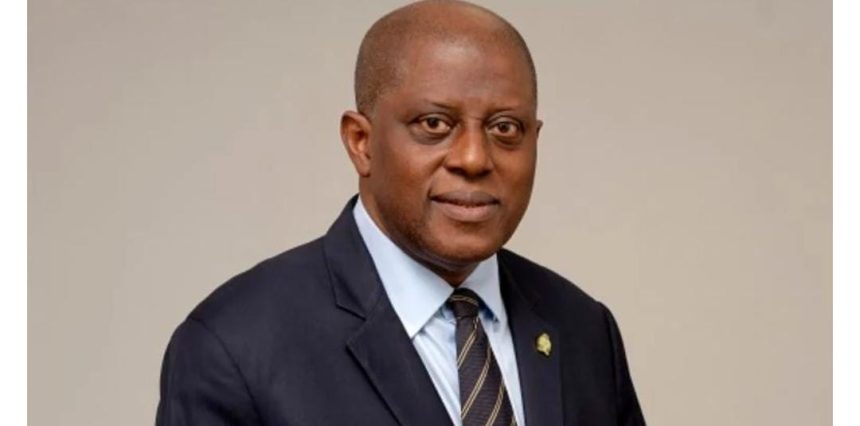

Under the new baseline standards issued by CBN Governor, Olayemi Cardoso, financial institutions must implement automated tools to detect, monitor, and report suspicious transactions in real time. Banks have 18 months to comply, while fintech companies and other financial service providers have up to 24 months. Institutions are required to submit detailed implementation roadmaps within three months.

The policy aims to enhance detection of illicit financial flows, improve investor confidence, and attract foreign capital. Automated AML systems leverage analytics, data monitoring, and artificial intelligence to flag suspicious activity and reduce vulnerabilities to money laundering, terrorism financing, and proliferation financing.

The move follows Nigeria’s removal from the Financial Action Task Force (FATF) grey list, a decision hailed by Cardoso as a validation of the country’s reform trajectory. The FATF noted Nigeria’s efforts to strengthen AML/CFT frameworks, a development that improves its global financial credibility.

The CBN report also highlights the fintech sector’s transformative role in promoting financial inclusion, particularly in underserved communities. With rising mobile phone penetration, fintech innovation can bridge the gap between traditional banking services and unbanked populations, supporting broader economic growth.

Cardoso emphasized the importance of balancing innovation with regulatory oversight, ensuring financial system integrity while fostering fintech-led inclusion.“Fintech must help deliver financial services to the last mile, from bustling cities to rural villages, so that no Nigerian is left behind in the digital economy,” he said.

The report identifies fintech segments spanning digital payments, lending, crowdfunding, InsurTech, WealthTech, and RegTech, noting that robust collaboration between regulators and innovators is essential for sustainable sector growth.

By combining regulatory rigor with technological innovation, Nigeria aims to position itself as a model for fintech leadership in Africa and globally, while maintaining a secure and resilient financial system.